WORKPLACE POSTERS

The U.S. Department of Labor (DOL) enforces the posting of employee notices in the workplace to comply with various DOL statues. The posters are available for free in multiple languages.

To determine which posters are needed for your business, the DOL FirstStep Poster Advisor can help. Employers can download and print the posters directly from the Advisor. It’s important to note that the Poster Advisor covers federal requirements, and for state-specific regulations, employers should refer to their state Department of Labor.

EMPLOYER SHARED RESPONSIBILITY PROVISIONS

Under the Affordable Care Act’s (ACA) employer shared responsibility rules and reporting requirements, status as an applicable large employer (ALE) is determined yearly. Employers that had an average of 50 or more full-time employees, including full-time equivalent employees, in 2023, are considered to be an ALE for 2024 and must meet reporting requirements by early 2025.

For plan years beginning in 2024, ALEs must offer at least one “affordable” health plan. Coverage under an employer-sponsored plan is considered affordable if the employee’s contribution is less than 8.39 percent of their household income for the taxable year. This formula is based on the cost of single coverage in the employer’s least expensive plan.

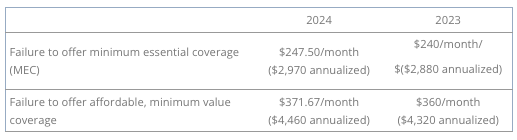

Penalties for ALEs that fail to offer affordable coverage have increased in 2024. These penalties may apply if an ALE fails to offer health coverage to a full-time employee and are assessed on a monthly basis. The amounts are based on the Department of Health and Human Services (HHS) inflationary percentage in its annual standards and the Internal Revenue Service’s official release for the year.

STATE INDIVIDUAL MANDATE REPORTING

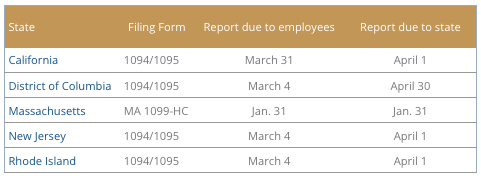

California, the District of Columbia, Massachusetts, New Jersey, Rhode Island, and Vermont have recently implemented individual mandate laws. These laws require that residents maintain minimum essential coverage (MEC) or face a state tax penalty. Additionally, certain states require entities providing MEC to submit information returns to the respective state revenue departments.

Most of these states accept the same Form 1094 and 1095 series used for federal MEC filing. Recently, various state revenue departments have issued updates concerning these reporting obligations, as detailed in the charts below.

Unlike many other employment laws, these state individual mandates do not hinge on the place of employment. Instead, the determination of whether these laws apply is based on the individual’s state of residence.

FEDERAL RECORD RETENTION REQUIREMENTS APPLICABLE TO GROUP BENEFITS

As the year ends, employers should review both federal and state retention guidelines for their employment-related records pertaining to group benefits. Maintaining the confidentiality of employee-related records is of utmost importance. Employee files must be treated with strict confidentiality and stored securely. Access to these records should be limited to individuals with a legitimate need to know or as mandated by law. Preserving the confidentiality of employee-related records aligns closely with decisions regarding the location, method, and duration of record retention.

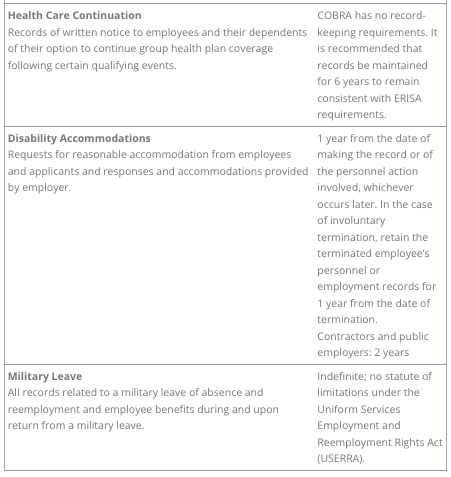

The chart below outlines federal guidelines for retaining employee files and other employment-related records pertaining to group benefits. Individual states may have additional requirements not covered here, so employers need to examine state employment laws related to recordkeeping and retention. Some of the listed requirements are applicable to a broad range of employers, while others specifically pertain to government contractors and subcontractors. Employers should carefully assess the laws to understand their coverage and corresponding responsibilities.

QUESTION OF THE MONTH

Q: We recently sent information to our clients about the Gag Clause requirements (whether insurance companies will handle or if they have to do any reporting themselves) and we were asked whether this has to be done for health reimbursement arrangement (HRA) plans since they are also self-funded.

A: The IRS, Department of Labor, and Department of Health and Human Services issued FAQs in February 2023. In the FAQs, the Departments acknowledged that an HRA is a self-funded health plan, however the Departments will not enforce the attestation requirement against plans that consist solely of an HRA. This is due, in part, because most HRAs are integrated with other coverage that will be required to do its own attestation. (See Q&A 8.)

Answers to the Question of the Week are provided by Kutak Rock LLP. Kutak Rock provides general compliance guidance through the UBA Compliance Help Desk, which does not constitute legal advice or create an attorney-client relationship. Please consult your legal advisor for specific legal advice.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. | |

| ©2024 United Benefit Advisors |